The cheapest commercial insurance you can find might be the most expensive mistake you ever make.

For a small business owner in Virginia, a low premium feels like a win — but it often excludes the very risks your specific business is most likely to face. This creates dangerous blind spots in your financial safety net that can surface at the worst possible moment.

At 360 Alchemist, we don't advise our clients to chase ghost commercial insurance policies — coverage that looks complete on paper but disappears when you need it most. We believe in providing coverage you can count on, while still finding premiums that fit your budget.

The Coverage Gap Most Virginia Small Businesses Don't Know They Have

Imagine you run a small marketing agency in Virginia. You have a General Liability policy, which covers "slip-and-fall" accidents in your office. Then a client sues for $50,000 over a costly typo in an ad campaign — and you discover your policy covers physical harm, not financial harm from your professional services.

This is a classic coverage gap. The fix is a separate policy for professional mistakes called Errors & Omissions (E&O) insurance — and most small business owners don't know they need it until it's too late.

This scenario illustrates how a business can be underinsured even when it has "checked the box." Policies required by a landlord or a client are a starting point — not a complete protection plan. Avoiding common small business insurance mistakes means understanding what your operation truly needs, not just what someone required you to buy.

A Real Example: Helping a Virginia Brewery Get Properly Covered

360 Alchemist worked with Eavesdrop Brewery in Manassas, Virginia, to help owner Frank find an affordable and complete commercial insurance package.

Because Eavesdrop serves alcohol, Frank needed more than a standard General Liability or restaurant insurance policy — he also needed liquor liability coverage, which can be expensive and is frequently overlooked.

We worked with multiple insurance brokers across Northern Virginia, and ultimately secured Frank a comprehensive, affordable commercial insurance package through RightAway Insurance that covered everything his business required.

This is what a business consultant does that an insurance broker typically doesn't: we start from a complete picture of your risks before anyone mentions a policy name.

Your Consultant as a "Risk Detective" for Your Virginia Business

Before we mention a single policy, we put on our detective hat. Our first job isn't to find you insurance — it's to understand your business inside and out.

You might think you just need coverage for theft or a customer lawsuit. But the biggest threats are often the ones you haven't considered. This deep-dive process is the foundation of effective business risk management for Virginia small businesses, and it's what separates a tailored plan from a generic, off-the-shelf policy.

This process — often called a risk assessment — uncovers the specific ways your business could suffer a financial loss. We examine your daily operations, equipment, employees, and physical location to build a complete picture of your exposure.

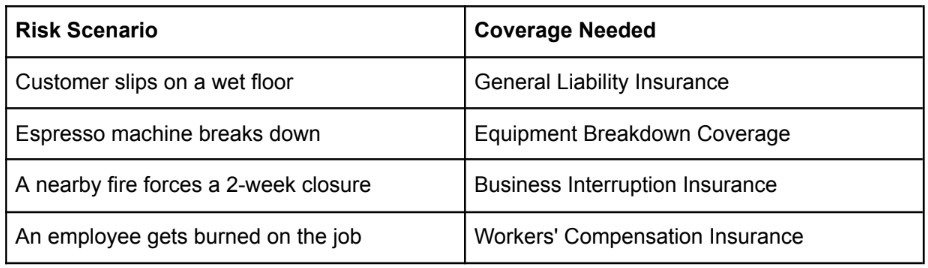

Example: A Coffee Shop's Risk Checklist

Armed with this analysis, your consultant builds a coverage blueprint — a clear, prioritized list of exactly what protection you need and why. It's the single most valuable tool you can have when shopping for commercial insurance in Virginia.

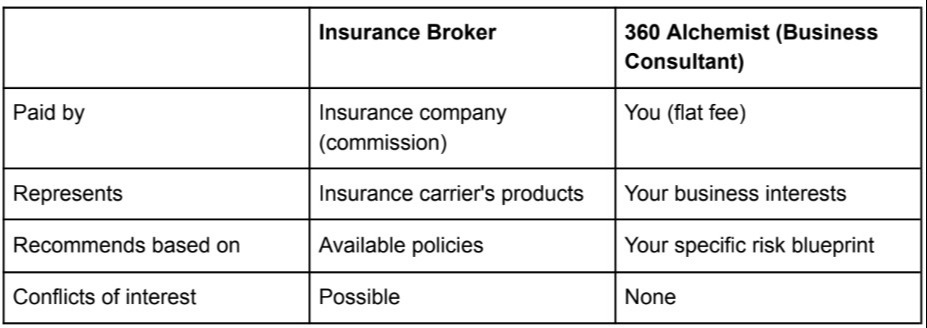

Consultant vs. Broker: Who Actually Works for You?

Once your coverage blueprint is complete, you'll work with an insurance broker to find actual policies. Here's what most small business owners don't realize:

Insurance brokers earn commissions. A broker earns a percentage of your premium — paid by the insurance company — when you buy a policy. Their incentive is tied to the sale.

360 Alchemist operates differently. We are Virginia business consultants working on a fee-for-service model. You pay us directly for expert advice, the same way you'd pay an accountant or an attorney. We don't sell insurance products, and we don't accept commissions from insurance carriers.

This distinction matters enormously: when advice isn't tied to a sale, you can trust it's centered entirely on what's best for your business.

Key Difference at a Glance

How an Independent Virginia Business Consultant Can Lower Your Insurance Costs

Beyond clarity, an independent consultant's greatest value is often measurable cost savings. Here's how:

1. Right-sizing your coverage. Many Virginia small business owners overpay by purchasing policies with coverage limits far exceeding their actual needs. Using your risk blueprint, a consultant helps you pay only for the protection you genuinely require.

2. Presenting you as a low-risk client. Insurance premiums are based on how risky underwriters perceive your business to be. A consultant packages your story — your safety procedures, claims-free history, and operational controls — to present you as a low-risk client. This can directly lead to lower premiums.

3. Creating competitive bidding. Your consultant gives multiple brokers the exact same information to bid on, forcing them to compete for your business on a level playing field. This prevents you from being steered toward a policy that serves a broker's commission more than your needs.

While a consultant charges a fee for this expertise, many Virginia small business owners find the cost is recovered in the first year through premium savings alone — making it a sound financial investment.

Beyond the First Policy: Long-Term Protection as Your Business Grows

Getting the right policy is a major win. But your business doesn't stand still — and neither should your coverage.

Over the next year, you might:

- Hire your first employee

- Launch a new online service

- Invest in expensive equipment

- Add a catering or delivery operation

Each of these positive steps can quietly create new insurance gaps, leaving you exposed without realizing it.

The Annual Policy Review

Think of an annual coverage review as a yearly check-up for your business's financial health. Your consultant revisits your operations, compares them against your current policies, and identifies any mismatches before they become costly problems.

Claims Advocacy

If you ever need to file a claim, a consultant can serve as your advocate — helping you organize documentation, understand the process, and communicate effectively with your insurance company during a stressful time.

This is the difference between a one-time transaction and a long-term protection partnership.

Frequently Asked Questions: Commercial Insurance for Virginia Small Businesses

- Most Virginia small businesses need, at minimum, General Liability insurance. Depending on your industry, you may also need Professional Liability (E&O), Workers' Compensation, Commercial Property, Business Interruption, and industry-specific policies like Liquor Liability for businesses that serve alcohol.

- An insurance broker represents insurance carriers and earns a commission when you buy a policy. A business consultant like 360 Alchemist represents you — working on a flat fee with no commission, so our recommendations are never influenced by a potential sale.

- A professional risk assessment — conducted by an independent business consultant — is the most reliable way to identify gaps. This process examines your operations, services, employees, location, and industry-specific risks to uncover blind spots standard policies often miss.

- 360 Alchemist primarily serves small businesses across Virginia, with a strong focus on Northern Virginia communities including Manassas, Arlington, Alexandria, Fairfax, and the broader DMV area.

- A ghost insurance policy is a policy that technically exists but provides no real protection when a claim is filed — often due to exclusions, insufficient limits, or mismatched coverage types. 360 Alchemist helps Virginia small businesses avoid ghost policies by building a coverage blueprint before purchasing any insurance.

- 360 Alchemist operates on a transparent, fee-for-service model. Unlike brokers, we charge a direct consulting fee rather than earning commissions — so the cost is clear upfront, and there's no hidden incentive to recommend more expensive coverage.

Your 3-Step Plan to Insurance Confidence as a Virginia Small Business Owner

You no longer have to view commercial insurance as a confusing maze of policies and premiums. Here's how to get started:

Step 1: Conduct a self-assessment.

Ask yourself these questions right now:

- Do I know exactly what my current policies cover — and what they exclude?

- What is the single biggest risk to my business? Am I covered for it?

- When was the last time an independent expert reviewed my coverage?

Step 2: Build a coverage blueprint. Work with an independent business consultant to identify your specific risks before approaching any broker. This blueprint becomes your shopping guide — ensuring you get the right coverage, not just coverage.

Step 3: Shop with an advocate. Let your consultant present your business to multiple brokers simultaneously, creating genuine competition and ensuring your protection plan serves your interests — not a broker's commission.

The goal isn't to check a box. It's to build a fortress around the business you've worked so hard to create.

360 Alchemist is a Virginia-based business consulting firm serving small businesses across Northern Virginia. We help business owners navigate commercial insurance with clarity, confidence, and coverage they can count on. Contact us to schedule your risk assessment.